Every REIT asset management team running a large portfolio eventually confronts the same analytical dilemma: how do you value 400 assets with sufficient precision to support institutional reporting while managing the cost and time constraints of a real-world team?

The two canonical approaches — portfolio-level regression models and asset-by-asset individual valuations — each have well-documented failure modes that become acute as portfolio size grows beyond 200-300 assets. This piece documents those failure modes and proposes a hybrid architecture that addresses both.

Portfolio-Level Regression: The Speed Advantage and Its Costs

Portfolio-level regression models estimate asset values by fitting a statistical model to a set of portfolio-wide characteristics — asset class, vintage, geography, size — and using that model to produce value estimates for every asset simultaneously. The key advantages are speed (a single model run produces values for all assets) and internal consistency (the model applies the same assumptions uniformly across the portfolio).

The failure mode is precision on the tails. Any portfolio-level model will fit the bulk of the distribution well — the standard multifamily asset in a typical submarket — while systematically misfitting the outliers: the suburban office that has been repositioned, the industrial asset in a micro-market with unusual characteristics, the NNN retail that has a credit-impaired anchor. Outlier assets are precisely the ones that carry the most valuation risk — a 10% error on 20 average assets is less consequential than a 30% error on 5 unusual ones.

The regression model's coefficient set is calibrated to the bulk of the distribution. It will estimate an average submarket industrial asset within 5-8% of market value. It will misestimate an unusual asset — one with idiosyncratic characteristics that the model's feature set doesn't capture — by 15-30%, with no signal in the output to indicate that the estimate is unreliable.

Asset-by-Asset Models: The Precision Ceiling at Scale

Asset-by-asset individual models — whether analyst-built DCFs, individual income approach models, or automated per-asset valuation systems — apply dedicated analysis to each property. For small portfolios (under 100 assets), this is the clearly correct approach. For large portfolios, it runs into a scalability ceiling.

The primary constraint is analyst time. A competent analyst building individual income approach models can cover approximately 8-15 assets per week with adequate depth. For a 300-asset REIT portfolio, a quarterly revaluation cycle requires 20-37 analyst-weeks of effort — approximately half the annual capacity of a 2-3 person dedicated portfolio valuation team. This is feasible but leaves little bandwidth for deal screening, tenant analysis, and the other responsibilities of the same team.

Automated per-asset systems address the analyst time constraint but introduce a different scalability problem: run time for high-precision per-asset models can become material at large scale. A system that takes 4 minutes per asset requires 20 hours to process 300 assets — which is fine if you can run it overnight, but becomes a constraint if you need real-time sensitivity analysis across the portfolio.

The Failure Mode Matrix

The choice between portfolio-level and asset-by-asset models creates different risk distributions depending on portfolio characteristics:

- Portfolio-level regression is dangerous when: The portfolio contains more than 15-20% "unusual" assets (assets that differ meaningfully from the model's training distribution), when the portfolio has heavy geographic concentration in a market the model was not primarily trained on, or when the portfolio has undergone significant transformation (repositioning, renovation, lease restructuring) that has changed its characteristics relative to the model's feature set.

- Asset-by-asset models are dangerous when: The portfolio is large enough that not all assets receive adequate depth of analysis, when different analysts use different methodologies for different asset types (producing inconsistent assumptions across the portfolio), or when the system applies the same high-precision model to asset types or markets where the underlying data quality doesn't support the precision being claimed.

Portfolio-level regression sacrifices precision on tails for speed. Asset-by-asset models scale poorly past 300 properties. Both failure modes create reporting risk that neither approach alone can resolve.

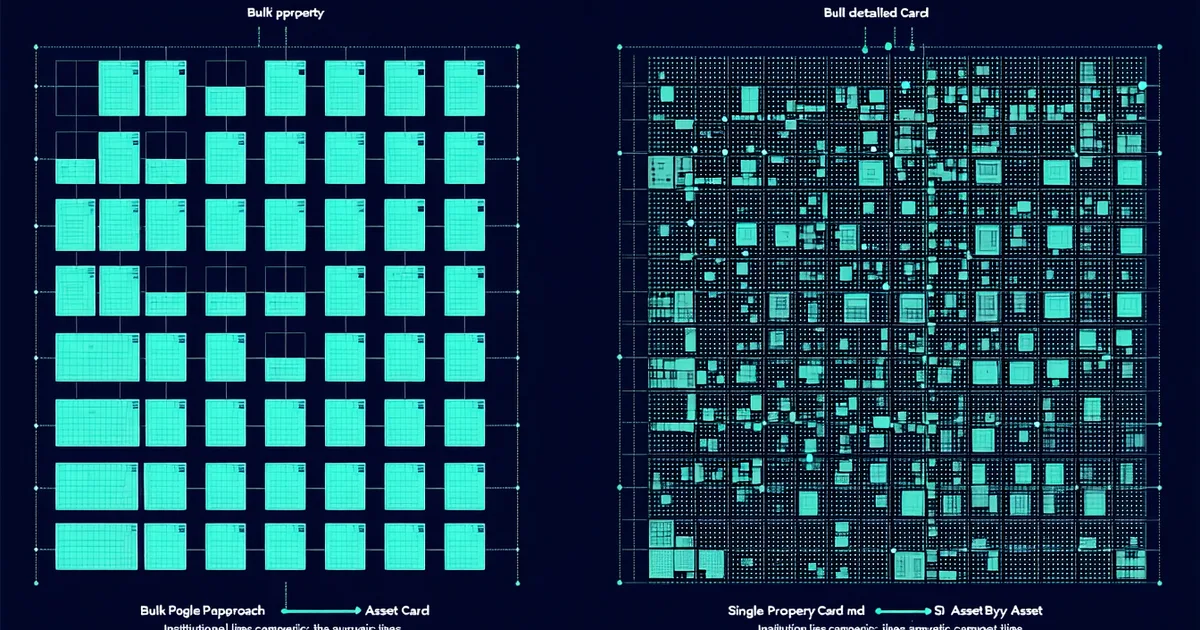

A Hybrid Architecture: Tiered Coverage by Asset Complexity

The hybrid approach segments the portfolio by asset complexity and applies appropriate methodology depth to each segment. The fundamental insight is that not all assets require the same analytical depth — the standard suburban industrial asset in a robust data market can be accurately valued with a quick automated run, while the ground-leased CBD office tower requires formal appraisal regardless of your time constraints.

Tier A: Standard Assets in Active Markets

Definition: Assets in property types and markets with robust comparable transaction evidence, operating under standard lease structures with no unusual characteristics.

Examples: Standard multifamily in major metros, Class B industrial in Tier 1 logistics markets, NNN retail with national credit tenants, stabilized suburban office in markets with recent comparable transactions.

Recommended approach: Automated per-asset valuation, quarterly cadence. The comp pool for these assets is deep enough that automated models produce tight confidence intervals. Annual formal appraisal for regulatory compliance, with automated quarterly estimates serving as the monitoring layer.

Estimated coverage in a diversified REIT: 55-65% of assets by count.

Tier B: Non-Standard Assets or Thin-Market Locations

Definition: Assets with unusual characteristics, in thin transaction markets, or undergoing operational change (renovation, lease-up, repositioning).

Examples: Value-add acquisitions mid-renovation, assets in tertiary markets with fewer than 5 same-submarket comps in the past 24 months, assets with lease rollover of more than 30% of GLA in the next 12 months, assets with concentrated speculative-grade tenancy.

Recommended approach: Automated valuation with enhanced analyst review, quarterly cadence. Analyst reviews the confidence interval, comp selection, and NOI assumptions specifically — the automated output is a starting point, not a final determination. Annual formal appraisal.

Estimated coverage: 25-30% of assets by count.

Tier C: Complex or Transitional Assets

Definition: Assets where standard income capitalization or comp stacking cannot produce reliable estimates — ground leases, development projects, conversion candidates, major repositioning.

Examples: Ground-leased assets with impending reappraisal resets, office-to-residential conversion projects in entitlement, assets in active litigation or receivership, development parcels.

Recommended approach: Formal USPAP appraisal, semi-annual or as events dictate. Automated models flag these assets but do not generate primary value conclusions for reporting purposes.

Estimated coverage: 5-15% of assets by count, but often 15-25% of portfolio value (complex assets tend to be larger).

Implementation: Building the Tiering System

The tiering classification should be done at the portfolio manifest level before the first automated run. Key classification criteria:

- Market data depth: How many same-submarket, same-type comparable transactions exist in the past 24 months? Fewer than 5: Tier B or C. Five to 14: Tier B. 15+: Tier A.

- Lease structure: Ground lease or unusual lease structure → Tier C. Standard fee simple with standard leases → eligible for Tier A or B based on other criteria.

- Operational status: Value-add in process → Tier B. Fully stabilized → eligible for Tier A based on other criteria.

- Confidence interval from automated run: Width of the confidence interval on the automated output is a direct indicator of appropriate tier. Interval width >15% → Tier B minimum. >25% → Tier C.

The tiering classification should be reviewed at each quarterly cycle and updated when assets change their operational or market status. A Tier B value-add asset that completes renovation and stabilizes should be reclassified to Tier A; a Tier A asset where a major anchor lease expires should be reclassified to Tier B or C pending lease resolution.

The Consistency Problem: Making the Hybrid Output Reportable

The main challenge in a hybrid approach is ensuring that the output is methodologically consistent enough to be reported as a single portfolio valuation rather than as a patchwork of different methodologies. For LP reporting and regulatory purposes, consistency across the valuation date is important.

The practical resolution is to use the automated quarterly run as the primary output for Tier A assets and as a baseline input for Tier B analyst review, while clearly documenting the methodology applied to each asset. The formal appraisals for Tier C assets should be conducted on the same date as the automated runs where possible, producing a unified quarterly snapshot across the full portfolio.

A portfolio NAV summary that includes a clear description of the methodology applied to each tier — "Tier A: automated comp-adjusted NOI model, N=185 assets; Tier B: automated model with analyst overlay, N=85 assets; Tier C: formal USPAP appraisal, N=30 assets" — is transparent about the analytical approach and gives the LP committee the context to evaluate the valuation quality.

The Economics of the Hybrid Approach

For a 300-asset REIT portfolio with the tier distribution described above:

- Annual formal appraisal cost (all assets): $900K-$2.4M at $3,000-$8,000 per asset

- Hybrid program (formal appraisals for 15% Tier C assets only + automated for Tier A/B): $135K-$360K in formal appraisal fees + automated platform subscription cost. Annual savings: 70-85% of traditional appraisal expenditure while achieving more frequent monitoring for 85% of the portfolio.

The hybrid approach is not a cost-cutting exercise at the expense of quality — it redirects formal appraisal expenditure toward the assets that genuinely require it while enabling more frequent, more current valuation for the assets that automated methods can handle reliably. For a 300-asset REIT, this is the correct allocation of analytical resources.